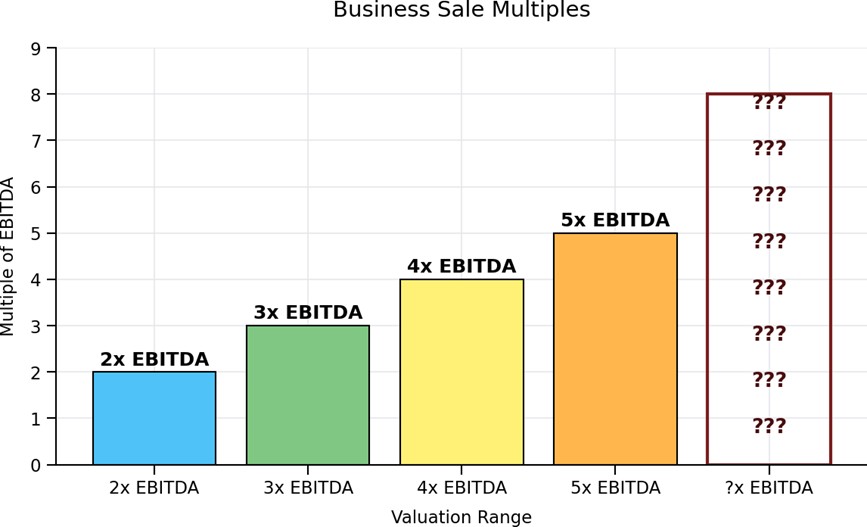

In the lower middle market, valuation conversations often begin and end with a multiple of earnings. Whether framed as a multiple of EBITDA, SDE, or adjusted cash flow, this provides a convenient benchmark for both buyers and sellers. However, synergistic buyers sometimes deviate from “standard multiples” and are willing to pay a premium. Understanding why this might occur, or if it even can occur, is essential.

At its core, a buyer might pay a premium over a typical multiple when they perceive incremental value unique to their situation. This value is not inherent in the business alone—it is realized through the buyer’s ability to leverage assets, capabilities, or strategic advantages in ways the current ownership cannot. Without that differential capability, there is little justification for a premium price.

One common driver of premium valuations is strategic fit. A buyer operating in the same or adjacent industry may be able to integrate the target company into an existing platform. This can create immediate synergies, such as cross-selling opportunities, expanded geographic reach, or increased purchasing power with suppliers. For example, a regional operator acquiring a competitor may eliminate redundant overhead, consolidate facilities, or improve pricing through scale. These efficiencies directly enhance profitability post-acquisition, allowing the buyer to justify a higher upfront price.

Another important factor is the potential for revenue expansion. Some buyers bring established sales infrastructure, marketing expertise, or distribution channels that the current owner has not fully utilized. A business with strong products but limited sales reach can be significantly more valuable in the hands of a buyer who can accelerate growth. The premium, in this case, reflects anticipated future earnings that are achievable specifically because of the buyer’s capabilities.

Intellectual property (IP) and proprietary processes can also command higher valuations, particularly when they are underexploited. A buyer with technical expertise or capital resources may be able to scale production, enhance product development, or commercialize innovations more effectively than the current owner. Again, the key is not the asset’s existence itself, but the buyer’s ability to extract additional value from it.

Customer concentration and relationships are often viewed as risks, but in the right context, they can be sources of premium value. A buyer with complementary offerings may deepen relationships with existing customers, increasing share of wallet and reducing churn. Similarly, long-term contracts or recurring revenue streams may be more valuable to a buyer with a lower cost of capital or a longer investment horizon.

Human capital is another frequently overlooked driver. A strong management team, specialized workforce, or unique company culture can be significantly more valuable to a buyer who knows how to retain and incentivize that talent. In contrast, an owner-operator model with limited delegation may suppress value unless the buyer has a clear plan to institutionalize operations.

Finally, differences in access to capital and the cost of capital can influence willingness to pay. Financial buyers or well-capitalized strategic acquirers may accept lower initial returns if they have confidence in long-term value creation. Lower financing costs or alternative capital structures can support higher purchase prices without compromising target returns.

Across all these factors, a consistent principle applies: a buyer will pay a premium only if they can do something with the business that the current ownership has not done or cannot do. And the buyer must be able to justify any premium paid by demonstrating that it increases profits accordingly. This may involve operational improvements, strategic integration, market expansion, or financial optimization. Without that incremental capability, the business remains valued on its current earnings profile, and the standard multiple prevails.

For sellers and advisors, the implication is clear. Identifying and articulating these potential value drivers—and aligning them with the right buyer profile—can materially impact transaction outcomes. The goal is not simply to demonstrate what the business is, but to highlight what it could become in the hands of a synergistic acquirer.